Skip to main content

Skip to main content

How to unlock more tax-free cash from your pension

As the landscape of pensions continues to evolve, understanding the nuances of regulatory changes is paramount for maximising tax efficiency and optimising your financial plans.

One recent development is the introduction of Transitional Tax-Free Amount Certificates, which offer a bespoke approach to deductions from the Lump Sum Allowance and Lump Sum and Death Benefit Allowance.

Arrange your free initial consultation

But if this all sounds like jargon and hard to wrap your head around, lets us better explain as we delve into the intricacies of these certificates, examining eligibility criteria, potential benefits, and potential drawbacks. Our primary focus will be on illustrating how these certificates can potentially benefit Defined Benefit pension holders (also known as a final salary scheme, but also include public sector schemes for example, Career Average Revalued Earnings or CARE) through a detailed calculation demonstrating the potential impact on their tax-free cash entitlement at retirement.

What are Transitional Tax-Free Amount Certificates?

Transitional tax-free amount certificates serve as tools to accurately reflect tax-free lump sums received before April 6, 2024, within the new pension framework. They are issued by registered pension schemes, allowing members to increase the level of tax-free cash available to them.

The Lump Sum Allowance sets the tax-free lump sum a pension holder can withdraw from their pension pot during their lifetime. This is currently standardised at £268,275; however, this can vary depending on individual protections. Pension Protections were introduced to protect pension savings from previous reductions in the Standard Lifetime Allowance.

The lump sum and death benefit allowance governs the tax-free lump sum payments beneficiaries can take following the pension holders passing and is currently set at £1,073,100. However, this may be reduced by tax free lump sums already taken by the member.

For individuals who accessed their benefits post-April 5, 2024, a standard transitional calculation is used to ensure adjustments are made to the lump sum allowance and lump sum and death benefit allowance. In most cases this standard calculation effectively reflects past benefits utilised and aligns correctly with the new regulatory framework. However, in certain circumstances, some individuals may qualify for a higher allowance by applying for a transitional tax-free amount certificate.

For Defined Benefit Pension Scheme members, two such circumstances are as follows:

- Members of Defined Benefit Pension Scheme where they opted to take a full scheme pension and did not receive a tax-free lump sum.

- Members of a Defined Benefit Pension Scheme who received a tax-free lump sum which was less than 25% of the pension’s value for lifetime allowance purposes (calculated as 20x the pension, plus any tax-free lump sum).

In these circumstances transitional tax-free amount certificates may offer a bespoke adjustment to the lump sum allowance and lump sum and death benefit allowance, ensuring a more accurate representation of the individuals tax-free lump sum entitlement. By accounting for actual lump sum benefits received, before the regulatory shift, transitional tax-free amount certificates provide a tailored approach that may prove advantageous for some pension holders.

Impact for Defined Benefit Pension Holders:

Here we will provide an example situation to further clarify how transitional tax-free amount certificates could provide a benefit to an individual who has taken tax-free cash under the 25% from their Defined Benefit Scheme.

Scenario:

Tom decided to begin drawing income from his Defined Benefit Pension t in 2020/2021. He took pension income of £27,500 per annum and chose to take tax free cash of £50,000.

If we assume Tom has Fixed Protection 2012 (giving him a Lifetime Allowance of £1,800,000) taking these benefits used up 33.33% of his Lifetime Allowance (£27,500 x 20, plus £50,000 = £600,000 which is 33.33% of £1,800,000).

| Without a transitional tax-free amount certificate | With a transitional tax-free amount certificate |

|---|---|

The standard calculation deducts 25% of 33.33% of £1,800,000 = £149,985 from his Lump Sum Allowance (LSA) and Lump Sum and Death Benefit Allowance (LSDBA) to give allowances available to use from 6 April 2024 of:LSA = £450,000 - £149,985 = £300,015

|

As £50,000 of tax-free cash was taken, £50,000 is deducted from the Lump Sum Allowance (LSA) and Lump Sum and Death Benefit Allowance (LSDBA) so the allowances available to use from 6 April 2024 are:LSA = £450,000 - £50,000 = £400,000

|

As this example explores, if you have not taken your full tax-free cash entitlement, you could be entitled to a larger lump sum allowance and lump sum and death benefit allowance by applying for a transitional tax-free amount certificate. This could allow you to take more tax-free cash from any other pension schemes you may hold and the implications of this could be significant. In this example, c. £100,000 of additional tax-free cash could be available to the individual, though please note this is still based on 25% of the value of any pension funds from which tax free cash has not yet been taken (for defined contribution pensions). Therefore a £400,000+ pension pot would be required to take full advantage of the additional tax free cash which is now available.

How to apply for transitional tax-free amount certificates:

Eligible individuals must submit a transitional tax-free amount certificates application to the pension scheme before taking any tax-free cash post-April 5, 2024. The success of a transitional tax-free amount certificates application hinges on the provision of complete and accurate evidence verifying the individual's entitlement to a reduced deduction from lump sum allowance and lump sum and death benefit allowance. Applicants must thoroughly compile documentation demonstrating their actual tax-free lump sum entitlements before April 6, 2024, ensuring compliance with regulatory requirements.

Potential pitfalls of applying for transitional tax-free amount certificates

While transitional tax-free amount certificates offer tailored adjustments to allowances, individuals must carefully evaluate the potential impacts on their pension benefits. Notably, calculations can vary significantly from individual to individual. For example, not everyone who took less than their 25% tax-free cash will benefit from applying for transitional tax-free amount certificates. In some cases, the issuance of a certificate may result in a reduction of allowances. If the outcome proves to be unfavourable creating less tax-free cash entitlement after applying for the certificate, this decision cannot be reversed.

How we can help

In this article we delved into the potential benefits offered to individuals with Defined Benefit pensions by the new Transitional Tax-Free Amount Certificates. If you believe this could be advantageous to you, it is important to seek financial advice before proceeding further. The possibility of this decision weakening your future pension position underlines the need for a comprehensive analysis of your previous benefits taken across your pension schemes.

At The Private Office we offer the guidance required to navigate these complex changes to pension legislation, ensuring that you are positioned optimally for your future and that you maximise the tax efficiency of the benefits you are entitled to. We can provide tailored financial advice to aid you in establishing the impact of transitional tax-free amount certificates on your specific situation, and we can assist you by preparing your application for potential submissions to your pension scheme providers, should these prove advantageous.

If you would like to schedule a call with one of our advisers, please get in touch. We can arrange an initial meeting at no cost and with no obligation, to further explore your own personal situation together.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate tax advice.

A pension is a long-term investment. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested.

The information in this article is based on current laws and regulations which are subject to change as at future legislations.

Government launches new state pension top up service

Those who have gaps in their National Insurance (NI) contributions can now top up their entitlement using a new government-backed online service.

The new payment service from HM Revenue & Customs (HMRC) and the Department for Work and Pensions (DWP) lets people see any gaps they have in their NI record and enables them to pay voluntary contributions to plug any holes so that they can access their state pension in full.

Historically, people have only been able to make voluntary contributions covering the past six years, but last year the Government extended this temporarily, meaning that anyone can make up NI gaps between April 6, 2006 and April 5, 2018. This temporary service will be available until April 5, 2025 as things stand.

Arrange your free initial consultation

How can I access my state pension?

In order to get access to a state pension when you retire you are required to pay at least 10 years’ worth of National Insurance Contributions (NICs). And for those wanting to claim the full amount of their state pension, which currently pays up to £221.20 a week (£11,502 a year), 35 years’ worth of NICs are needed.

Although widely agreed to be insufficient to cover sometimes even the basic cost of living alone, the UK state pension is nevertheless important to understand as currently it is a guaranteed source of income in retirement, provided you’ve made enough NI contributions. Additionally, due to the ‘triple lock guarantee’, the state pension currently increases each year in line with Consumer Price Index (CPI) inflation, average wages or by 2.5%, whichever is higher.

Plugging the gaps

Anyone can have gaps in their NICs. If you were unemployed, took time out to raise a family, in education or even if you were not earning enough, you may have periods where no NIC payments were made.

As mentioned, you need to have been paying NIC for at least 10 qualifying years in order to receive any kind of state pension, and you need to have been paying for a full 35 years to receive the full amount possible.

The new Government online service allows anyone to view their current state pension entitlement and to make up NI gaps between April 6, 2006 and April 5, 2018. But this opportunity is only available for a short period as you only have until April 5, 2025. This means that if you want to receive your full state pension and you have gaps going back further than six years, now is the time to think about plugging those gaps by purchasing missed years.

About National Insurance Contributions

National Insurance (NI) is an umbrella term for universal health care, unemployment benefits and the public pension program.

National Insurance Contributions (NICs) are a form of tax that employees and employers pay to the Government through payroll deductions. NICs are paid automatically through the PAYE (Pay As You Earn) system, which deducts an amount based on a percentage of your income, and this generally continues until you reach retirement age. Employees are able to make additional voluntary payments to increase the pension amount that they will be entitled to receive.

NICs are generally considered to be collected in order to fund various state benefits, such as the NHS and state pensions.

If you are thinking about your options at retirement, you can book a free non-committal initial consultation where you can discuss your plans with one of our accredited advisers who will be happy to guide you through the process. Alternatively, you can give us a call on 0333 323 9065 to get in touch with a member of our team to find out more.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

This article is based on our understanding of Government practice as at 6 April 2024.

How to plan your finances in an election year

The Rest is Elections

The British electoral system does not lend itself to coalition governments. Ask anyone from the Liberal Democrats how they feel about the Conservative/Lib Dem coalition of 2010 and they probably won’t refer to it in glowing terms. Historically, this means that the UK is subject, every now and then, to a lurch from right to left, or vice versa. With this lurch we tend to see fairly fundamental changes in policy. At least, we used to.

I don’t think I am being controversial by suggesting there is a strong possibility that Kier Starmer will be the next Prime Minister at some point this year. The last time we had a change from Conservative to Labour was Tony Blair’s victory, 27 years ago, in 1997, with a majority of 179. According to a recent poll, Labour is heading for a majority of 298! We’ll see. But already, many of our clients are thinking about what a Labour Government will mean for them and what, if anything, should they be doing to protect their finances.

Arrange your free initial consultation

For Financial Advisers, we are always in a difficult position when it comes to offering advice on an unknown. At the time of writing, the Labour manifesto has yet to be written and we are short of precise detail. Without a crystal ball it would be unwise for us, or any other adviser, to recommend a course of action based on speculation.

To a certain extent, we experience the same thing every year with the budget. I have been advising clients for over 35 years and every year I hear the same fears. Are we going to see the end of tax-free cash in pensions? Will higher rate tax relief on contributions be removed? Will any changes be retrospective? They are, in essence, the same fears as those before an election.

Will Labour tax the rich and give to the poor?

Labour, in blunt terms, has always been associated with taxing the rich and redistributing to the poor. The Labour administration of the 70s imposed an eye-watering top rate of income tax at 83% for those with incomes above £20,000 (£221,741 in today’s terms). With the investment income surcharge of 15% added, this resulted in the now famously high-water mark of 98%, the highest rate since the war.

I think it is worth pointing out that politics from the 70s was far more polarised than it is today. Tony Benn was openly attempting to nationalise virtually every British industry in sight, and the unions were hell bent on removing anyone from government who was more right wing than Che Guevara. If you haven’t done so already, I thoroughly recommend listening to the excellent ‘The Rest is History’ podcast ‘Britain in 1974’. Apart from highlighting this polarity, it is also a stark reminder of just how bad things had become.

Since the 90s the major parties have become (in historical terms at least) more centrist, and both Labour and Conservatives exhibit the same general desires when it comes to taxation and government debt. The current tax take (under the Tories) is the highest it has been since the war. The highest rate of income tax now is 45%, higher than it was under Labour in 2010. Admittedly, both parties have, in recent years, examined their political extremities (Corbyn for Labour and the Reform breakaway for the Conservatives) but the truth seems to be that monetarism has won the day and the days of ultra-high taxation and reckless borrowing seem to be history. At least for now.

How can you protect yourself?

So, returning to the steps our clients can take to protect their positions, in advance of the general election, I think it will probably focus on the peripheral subjects such as the Lifetime Allowance, or good savings fundamentals, which apply regardless of elections.

The Lifetime Allowance (LTA) has just been abolished, but as soon as its demise was announced, Labour publicly stated that they would reinstate it. But without knowing what shape this will take, it is impossible for us to advise. They could simply reinstate the previous level (£1,073,100). If this is the case, it may be in our clients’ interests to ‘crystallise’ their pensions above this figure beforehand. But what if they don’t? What if the LTA is increased to £1.8 million and tax-free cash is increased to 25% of this figure as a conciliatory gesture? In this case, you would be penalised by crystallising pensions now, up to this number. This is because there is now a new ‘Lump Sum Allowance’ (LSA) which is £268,275, and this represents the aggregate maximum amount of tax-free cash that can be taken from all schemes. There is also no guarantee that any change, whatever it might be, wouldn’t be retrospective.

So, what else might change? As I mentioned earlier, this is a question which also crops up every budget and the best protection anyone can take is probably to make the most of any tax breaks which are currently available.

First on the list is pensions. Obtaining tax relief on contributions is, and always has been, an extremely tax efficient move, especially for higher rate and, particularly, additional rate taxpayers. Not only do you receive tax relief on contributions (subject to annual allowance limits) but all pension funds grow free of capital gains tax and personal income tax. The pension fund is also outside of the estate for inheritance tax purposes.

ISAs are probably the next port of call with individuals permitted to invest up to £20,000 each tax year (plus a forthcoming British ISA allowing a further £5,000 each tax year). ISA funds are also free from capital gains tax and income tax which makes them superb retirement planning vehicles.

If a new government chooses not to change them then, well, they were a good idea anyway, and if they do change them (for the worse) then you have maximised tax efficiency beforehand (subject to there being no retrospective changes).

I think one thing is fairly certain. The UK is not in fine financial health and handouts will not be the order of the day. But like him or loathe him, Kier Starmer is no Tony Benn and, to quote Benjamin the donkey in Animal Farm, I suspect things will continue much the same as they did before. That is to say, badly!

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The opinions shared in this article are solely those of the individual and they do not necessarily reflect those of The Private Office.

Financial Conduct Authority does not regulate tax planning.

A pension is a long-term investment. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested.

The information in this article is based on current laws and regulations which are subject to change as at future legislations.

Which country has the best state pension?

Following the announcement that the state pension would rise by 8.5% this year, research from Standard Life showed that 22% of adults still don’t know what state pension they will be receiving. This rose to 29% for those aged between 55 and 64, which either demonstrates a lack of pension knowledge or a lack of concern for those already at pension age.

It’s no secret that the UK state pension is known for being insufficient for a complete source of income in retirement, often unable to cover even the basic costs of living. This situation has been exacerbated by rocketing inflation over recent years. However, even for those with higher incomes, the state pension remains a valuable additional income source and an essential one for those who earn little or no additional retirement income.

Arrange your free initial consultation

It’s worth remembering that not everyone gets the same state pension amount. How much you get depends on your National Insurance record. For many people, the State Pension is only part of their retirement income, as the maximum a person in the UK can receive from their state pension currently is £221.20 a week for the 2024/25 tax year. Instead, they may also have money from a workplace pension, other pension and/or earnings, which is increasingly essential.

Sadly, even those who are able to access the current maximum £11,502.40 a year are still almost £3,000 shy of what is considered, by the pension industry guidelines, to be the amount required to have a minimum standard of living. And following the Governments freeze on allowances, many more pensioners, even on low-income levels that push them over the annual allowance, will be paying more tax. In fact, charities including Age UK, have reported an increase in concern among pensioners who fear being dragged into paying income tax.

How the state pension compares across the world

While the state pension is certainly not enough to live on alone, it’s interesting to see what the state pension looks like in other major countries to get a complete picture of where the UK stands comparatively.

In the UK, if you have 35 years of National Insurance contributions, you are currently eligible to receive the full state pension amount of £958 a month. Between Australia, Denmark, France, Germany, the Netherlands, Spain and the United States, the UK has by far the lowest state pension, according to recent figures from This is Money. Most offer between the equivalent of £1,500 - £2,500 a month, with Spain offering the equivalent of £3,060, more than triple what the UK state pension pays to pensioners.

One reason for this is due to the UK’s flat-rate pension. You get the same amount regardless of earnings, while in many other countries the state pension is linked to your earnings. This means that while the maximum may be high in other countries that have pensions based on earnings, this would not necessarily be what the average pensioner would receive, with many receiving less than the flat-rate amount offered for UK pensioners. The flat-rate approach is more beneficial for those on low incomes and, by the same token, higher earners in the UK get less from the state pension than their international counterparts who are enrolled in systems based on what they earn.

Another point of comparison to consider is what is required to access these state pensions. In the UK, you are required to have 35 years’ worth of National Insurance contributions before you can access the modest state pension on offer. By contrast, the Netherlands, which offers a more attractive £1,230 a month, requires a full 50 years’ worth of National Insurance contributions. Even though the state pension is higher in the Netherlands, the extra 15 years of National Insurance contributions that you have to make, should not be understated.

If you’re thinking about or approaching your retirement and would like to speak to an expert to assist in mapping out your financial future, why not get in touch. We’re offering all of those with £100,000 or more in pensions, savings or investments a free initial consultation.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

This article is based on our understanding of Government practice as at 6 April 2024.

This article is accurate and correct as the time of writing 01/05/2024.

Can I withdraw money from my pension?

Pensions serve as a fundamental element of retirement planning, providing you with a source of financial security during retirement. Yet, navigating the evolving pension landscape, with ever-changing rules and regulations, alongside the array of retirement options available, can be daunting.

Questions inevitably arise such as “when can I access my pension?” and “what are my retirement options?”. Here we aim to address these questions, providing some clarity on how and when you can withdraw from your pension.

Arrange your free initial consultation

How to withdraw money from your pension

In the UK, there are generally two types of pensions that can be set up: defined benefit and defined contribution pensions.

- Defined benefit pensions (also known as a final salary scheme, but also include public sector schemes for example, Career Average Revalued Earnings or CARE) guarantee a fixed income in retirement determined by salary and length of service, with a degree of inflation protection built in.

- Defined contribution pensions build a fund through contributions from you, your employer, or both, with your retirement income dependent on the pot’s growth. Defined contribution schemes can be workplace or personal pensions and typically provide more flexibility with retirement options.

It is therefore important to understand the different options available to you.

Since the enactment of pension freedoms legislation (‘pension reforms’) in April 2015, accessing and managing your pensions has become more flexible. You can now access your defined contribution pension from the age of 55 (increasing to age 57 in 2028) with access to a wider range of options. While this flexibility is advantageous, it is important to understand the implications of each option and how any decision will impact your future.

What are my retirement options?

- Lump sum withdrawal(s) - Otherwise known as uncrystallised funds pension lump sum (UFPLS), this option allows you to either withdraw your entire pension as a cash lump sum all at once, or in stages (dependent on what your provider offers). The initial 25% will typically be tax-free (up to the standard lump sum allowance of £268,275), and the remainder subject to income tax. For larger pots, this could create a significant income tax liability. This approach provides flexibility by allowing you access to your funds when needed, while also maintaining investment possibilities and phasing your tax-free cash over the years. It is important to note that if you opt to cash in your pension entirely, you could miss out on future investment growth opportunities and face potential financial shortfall in later years.

- Purchase an annuity – An annuity provides a guaranteed income for life, allowing you to convert your pension pot into a reliable stream of payments over a lifetime or a predetermined period. You can opt to receive up to 25% of your funds tax-free upfront, with the remaining funds being used to purchase the annuity where the income you receive is taxable. You have the freedom to buy an annuity from any provider, not necessarily the one your funds are held with, although some may require a minimum investment. It is possible to build in annual annuity increases or protection for a spouse or other beneficiary, however, this reduces the starting level of income. It is worth noting though that once you purchase an annuity, the decision is irreversible, and you cannot change your mind and switch to another plan or provider.

- Pension drawdown – This option offers the greatest flexibility, allowing you to withdraw a tax-free lump sum of up to 25%, followed by regular taxable income, while keeping the remaining funds invested. You have the freedom to manage your investments and withdraw funds according to your needs and income tax position. Not all pension schemes or providers offer drawdown, so you may need to move to a different provider to facilitate this.

- Keep your pension pot as it is – Lastly, you do have the option to take nothing at all and keep your pension pot where it is which allows for continued investment growth. However, fluctuations in market performance can lead to your fund decreasing in value as well as going up. In all cases, it is also important to check the death benefits position on your current arrangements to ensure they are tax-efficient for your beneficiaries.

When can I access my pension?

The minimum pension age for accessing pension pots typically stands at 55 years. However, this is increasing to 57 from 6 April 2028, aligning with the planned increment in the minimum State Pension Age to 67 between 2026 and 2028.

Can I withdraw from my pension early?

Early withdrawal from your pension, typically before the age of 55, is primarily contingent upon your health status. If you are required to retire early due to illness, you may qualify for access to your pension pot before reaching the minimum age threshold. Eligibility varies from provider to provider, but usually applies when your health prevents you from continuing employment and earning income. Withdrawing funds before age 55 and without any qualifying circumstances incurs substantial tax charges.

Summary

As evident, there are various options available for withdrawing money from your pension, but it is essential to consider the implications of each option. Seeking advice from a financial adviser who can provide tailored advice based on your individual circumstances is therefore recommended.

We’re offering a free cash-flow plan worth £500 to all those with £100,000 or more in pensions, savings or investments. Find out more here.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

A pension is a long-term investment. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested.

The information in this article is based on current laws and regulations which are subject to change as at future legislations.

The big pension changes in 2024 and how to plan for them

2024 will see some huge changes to pensions, not least the much-publicised abolition of the Lifetime Allowance (LTA). So how do you prepare for a rapidly changing pension landscape? With a general election around the corner and the likelihood of a changing Government how can you plan for changes in legislation that could well be scrapped later down the line?

Arrange your free initial consultation

Lifetime Allowance

Taxation on pension funds has been a hot topic since the 2023 Spring Budget when the Chancellor announced his intention to abolish the ‘Lifetime Allowance (LTA)’. The LTA is the total value that someone can accrue within a pension over their lifetime without incurring certain tax charges. Under LTA rules you could face a tax charge of up to 55% on pension savings above £1,073,100. So, for people with large pension pots, the prospect of abolishing this allowance was welcomed.

The announcement also signposted the introduction of two new allowances which will restrict the amount of tax free lump sums which could be paid under the new pension regime from 6 April 2024.

The new Lump Sum Allowance is the upper limit on the tax-free cash someone can take from their pensions during their lifetime and is capped at 25% of the previous LTA (£268,275).

The second allowance, the Lump Sum and Death Benefit Allowance will restrict the tax free lump sum which can be paid from your pension funds to your beneficiaries if you die before your 75th birthday. The Lump Sum and Death Benefit Allowance is set at £1,073,100 and the new regulation does not have any provision for these to increase over time to keep pace with inflation.

If you had previously registered for one of the many forms of protection against the Lifetime Allowance and have not broken the conditions for maintaining your protection you will benefit from a higher Lump Sum and Lump Sum and Death Benefit Allowance.

To account for benefits taken between 6 April 2006 and 5 April 2024 a transitional calculation has been provided so that individuals can calculate their remaining available Lump Sum Allowance and Lump Sum and Death Benefit Allowance.

There is a secondary calculation which can be undertaken for individuals who did not receive the full tax free cash lump sum entitlement of 25% when pension benefits were taken previously which may enable them to receive an increased Lump Sum and Lump Sum and Death Benefit Allowance. It is advisable to take financial advice when undertaking these calculations as they can be complex.

As soon as the Chancellor announced the abolition of the LTA, Labour announced that they would reintroduce the LTA if they are elected following the impending General Election with the current Prime Minister, Rishi Sunak, suggesting this will happen in the second half of this year.

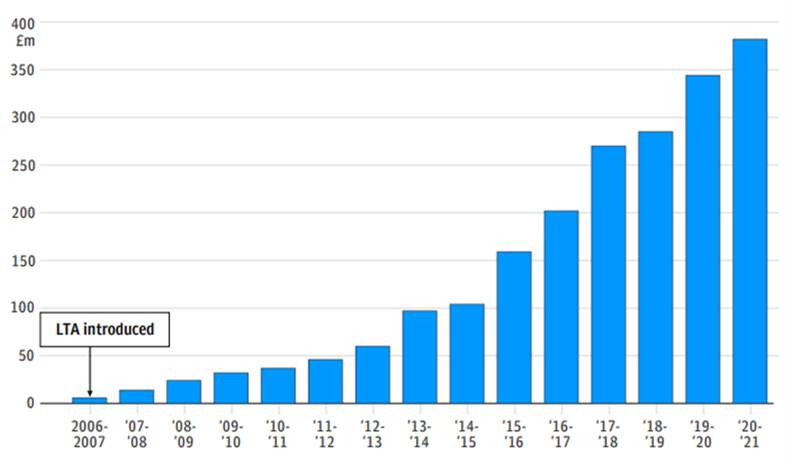

The number of people paying tax for breaching the LTA has been increasing in recent years (See Figure 1) , and the reintroduction of the limit after a period of overcontributing will push this number even higher. If the LTA is reintroduced at its previous level, it is estimated that around 250,000 people will be over the limit.

Figure 1: Tax Paid for breaching lifetime allowance, Source: HMRC, 2024

Many are concerned that bringing back the cap will push senior NHS doctors into an early retirement. One of the key motivations for scrapping the LTA initially was to deter NHS doctors from retiring early to avoid tax bills.

Could a Labour government reverse the rules?

In the run up to the election we could see a sudden flurry of savers rushing to draw down on their pensions before the potential reintroduction of an LTA. To prevent this, Labour may decide not to go ahead with the reversal.

Now that the legislation has been passed and HMRC have almost completed the implementation of the changes, tax experts have said it will be more difficult for policymakers to reverse the rules. This uncertainty leaves savers in a tricky position, as they try to second-guess the next move by a government.

So, do you make the most of the current pension rules or stay cautious in case Labour reverses the changes? In the past when the LTA has been changed HMRC has introduced protections for those who breached the new lower limit. Therefore, if the cap is reintroduced savers who are over the limit might be able to protect their pot. It is hard to predict how a new government might behave but many are hopeful for some form of protection.

If you are thinking about crystalising your pension early to avoid issues with a Lifetime Allowance tax charge, given the complexity of the matter, you should first consult your financial adviser.

Annual Allowance

It is also worth noting that the pension annual allowance changed from £40,000 to £60,000 on the 6th April 2023. Although there is not a limit on the amount that can be saved into pensions each year, there is a limit on the amount that can benefit from tax relief. The ‘Annual Allowance’ is the limit that an individual can contribute to a pension personally in any given tax year, whilst benefiting from tax relief.

For example, someone receiving a salary of £40,000, would only receive tax relief on personal contributions up to £40,000, but someone on a salary of £80,000, would only attract tax relief on contributions up to £60,000. It is important to note that lower limits apply to high earners or individuals who have already accessed some of their pension funds flexibly.

State Pension

The state pension is due to receive an 8.5% rise this month, taking it from £10,600 to £11,502 a year. This is the second largest percentage rise in the last 30 years. It is worth remembering that this isn’t the case for everyone who is entitled to the state pension, and there is no guarantee that the next government will retain the current “triple-lock” status afforded to the State Pension.

You can read more about specific pension details published in the Autumn Statement here.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The information contained within this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

Gender Pensions Gap continues

The new report from the Pensions Policy Institute revealed that the gap in pension value between men and women is still significant, with 67% of pensioners in poverty being women.

According to the report, a girl would need to start saving from 3 years old to match the pension of a man who began at 22, and a woman in her late 50s has approximately a third of the retirement savings of an average man of the same age.

This difference means that women are more likely to struggle financially in retirement than men. Even though the gender pensions gap shrank by 7% between 2006 and 2020, according to official figures, it remains a gender-based issue that continues to put pressure on the financial equality between the sexes to this day.

Arrange your free initial consultation

Only this week, there have been protests by Women Against State Pension Inequality (WASPI) - a voluntary UK-based organisation founded in 2015 that campaigns against the way in which the state pension age for men and women was equalised. They call for the millions of women affected by the poorly communicated change in pension age for women to receive compensation. The Parliamentary and Health Service Ombudsman ruled that those affected should be compensated. Depending on the numbers affected, the total bill could end up being in the billions of pounds – more than £10bn if all women born in the 1950s are compensated. The Prime Minister's spokesperson said that the Government would be taking time to consider the report, and it is unclear whether any actual payout will take place.

What is the gender pension gap?

The gender pension gap is the difference in pension savings, and then retirement income, between the genders. The research shows that men have substantially larger pension pots than women as they approach retirement, resulting in a significant difference in retirement security between the genders.

For men and women just beginning their career, the gender pension gap doesn’t exist. After all, we all start with an empty pension pot. Then men gradually take the lead until their early 30s where the gender pension gap actually shifts in the other direction – for those eligible for auto-enrolment – with women having larger pension savings than men.

After 35 is where the real gender pensions gap begins to emerge in favour of men. There is a 10% gender pension gap between the ages of 35 and 39. By late 40s, this has expanded to a huge 47%, according to the Government’s Gender Pensions Gap report.

Why does the gender pension gap exist?

There are a number of factors that contribute to the startling gap between the genders in pensions wealth.

Firstly, the gender pay gap, which naturally contributes to the difference due to women taking home less pay on average and therefore contributing less into their pensions.

Women historically perform the bulk of unpaid labour in society. For example, women are more likely to put their careers on hold while raising a family and they are more likely to work part-time, especially during the initial period of parent life. Data from the Office for National Statistics (ONS) showed that 38% of women were working part-time compared to just 14% of men in 2022. And while this is changing, with paternity leave becoming more common, it remains that women statistically are the ones that sacrifice their hours, and therefore their pensions contributions, in order to help raise a family.

Additional factors at play that contribute to the pensions gap include: career paths, gender pay discrimination, how pensions are split following divorce, to name but a few.

But the bottom line is, if you’re a woman, you’re statistically more at risk of having significantly less pension wealth than you should for a healthy retirement.

The key to avoiding these shortfalls is to plan in advance. Considering how all of these factors can affect your pension wealth down the road, planning accordingly can go a long way to mitigating some of these inherent disadvantages. Specifically, a female-focused retirement planning approach is the most effective way to secure a comfortable retirement.

If you’d like to find out more about how to navigate potential pension shortfalls, or are simply interested in finding out more about how you can best plan for the future of your pension, why not give us a call on 0333 323 9065 or book a free non-committal initial consultation with one of our experts to find out how we can help.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

Spring Budget 2024

The Spring Budget 2024 confirmed some rumours, such as the introduction of a British ISA, and at the same time, contained a few surprises too.

The main points are summarised below along with a reminder of some of the other changes coming into effect in April 2024.

Some measures are potentially subject to change until enacted into legislation.

If you have any questions or would like to speak to one of our expert financial advisers about the changes announced, contact us to arrange a free initial consultation.

Arrange your free initial consultation

Pensions

Abolition of Lifetime Allowance (LTA) from 6 April 2024

A further Pension Schemes Newsletter / Lifetime Allowance Guidance Newsletter is expected this week but no further detail was issued as part of the Budget itself. Further information will be issued once it’s available.

State pension

Triple lock means new state pension and basic state pension will increase by 8.5% in April 2024. Full new state pension figure will be £221.20 per week.

Investments

Individual Savings Accounts (ISA)

The annual subscription limits all remain at their current levels in 2024/25, i.e.

- £20,000 ISA

- £4,000 Lifetime ISA

- £9,000 Junior ISA (and Child Trust Fund)

A new British ISA is to be introduced from a date to be confirmed. This will give investors an additional £5,000 ISA allowance each tax year, so on top of the current £20,000. There is a consultation paper in place to obtain feedback from ISA managers, but the idea is for allowable investments to include UK equites and potentially UK corporate bonds, gilts, collectives.

As previously announced at the Autumn Statement, the government is to make changes to ISAs to simplify the scheme and widen the scope of investments that can be included in ISAs. To simplify the scheme the government will:

- Allow multiple subscriptions in each year to ISAs of the same type, from 6 April 2024

- Remove the requirement to make a fresh ISA application where an existing ISA account has received no subscription in the previous tax year, from 6 April 2024

- Allow partial transfers of current year ISA subscriptions between providers, from 6 April 2024

- Harmonise the account opening age for any adult ISAs to 18, from 6 April 2024

- Digitise the ISA reporting system to enable the development of digital tools to support investors

Reserved Investor Fund

The Reserved Investor Fund is a new type of investment fund designed to complement and enhance the UK’s existing funds rule. This meets the industry demand for a UK-based unauthorised contractual scheme, with lower costs and more flexibility than the existing authorised contractual scheme. The introduction date is still to be confirmed.

Taxation

Income tax

All income tax rates and bands remain at their current levels in 2024/25. See our latest tax tables 2024/25.

National insurance (NI)

National Insurance is paid by people between age 16 and State Pension age who are either an employee earning more than £242 per week from one job or self-employed and making a profit of more than £12,570 a year.

Following on from the NI cuts made in the Autumn Statement when the 12% rate of employee NI reduced to 10% from January 2024, the government is cutting the main rate of employee NI by 2p from 10% to 8% from 6 April 2024.

They are also cutting a further 2p from the main rate of self-employed National Insurance on top of the 1p cut announced at Autumn Statement and the abolition of Class 2.

This means that from 6 April 2024 the main rate of Class 4 NICs for the self-employed will now be reduced from 9% to 6%.

Child Benefit charge

The adjusted net income threshold for the High Income Child Benefit Charge (HICBC) will increase from £50,000 to £60,000, from 6 April 2024.

For individuals with income above £80,000, the amount of the tax charge will equal the amount of the Child Benefit payment. For those with income between £60,000 and £80,000, the rate at which HICBC is charged is halved, and will equal one per cent for every £200 of income that exceeds £60,000.

New claims to Child Benefit are automatically backdated by three months, or to the child’s date of birth (whichever is later). For Child Benefit claims made after 6 April 2024, backdated payments will be treated for HICBC purposes as if the entitlement fell in the 2024/25 tax year if the backdating would otherwise create a HICBC liability in the 2023/24 tax year.

In his Budget speech, the Chancellor announced that the plan is to move assessment for the HICBC to a system based on household income from April 2026. This is to remove the current unfairness meaning that a couple who each have income below the threshold, so could in 2023/24 have £49,000 pa each (£98,000 pa in total), wouldn’t be subject to the HICBC whereas another household with one person with income of £51,000 for example would.

Dividend allowance

As we are already aware, the dividend allowance reduces from £1,000 to £500 on 6 April 2024. Dividend tax rates remain the same at 8.75% in basic rate band, 33.75% in higher rate band and 39.35% in additional rate band (and 39.35% for discretionary trusts).

Arrange your free initial consultation

Capital gains tax (CGT)

Annual exemption reduces from £6,000 to £3,000 on 6 April 2024 (a maximum of £1,500 for discretionary/interest in possession trusts – shared between all settlor’s trusts subject to a minimum of £600 per trust).

CGT rates remain as they currently are apart from the higher CGT rate for residential property gains (the lower rate remains at 18%):

- 10% for any taxable gain that doesn’t fall above the basic rate band when added to income and 20% on any gain (or part of gain) that falls above the basic rate band when added to income

- For residential property gains these rates increase to 18% and 24% (formerly 28%) respectively

- Discretionary/interest in possession trustees and personal representatives pay at the higher rates (20%/24% (formerly 28%))

Simplifications for trusts and estates

From April 2024 trustees and personal representatives of estates will no longer have to report small amounts of income tax to HMRC and taxation of estate beneficiaries will be simplified, as shown below:

- Trusts and estates with income up to £500 will not pay tax on that income as it arises

- The £1,000 standard rate band (effectively basic rate band) for discretionary trusts will no longer apply

- Beneficiaries of UK estates will not pay tax on income distributed to them that is within the £500 limit for the personal representatives

Stamp duty land tax (SDLT)

SDLT Multiple Dwellings Relief is being abolished from 1 June 2024. This applies to purchasers of residential property in England and Northern Ireland who acquire more than one dwelling in a single transaction or linked transactions.

Changes to the taxation of non-doms

The concept of domicile is outdated and incentivises individuals to keep income and gains offshore. The government is therefore modernising the tax system by ending the current rules for non-UK domiciled individuals, or non-doms, from April 2025. A new residence-based regime will take effect from April 2025.

From April 2025, new arrivals, who have a period of 10 years’ consecutive non-residence, will have full tax relief for a 4-year period of subsequent UK tax residence on foreign income and gains (FIG) arising during this 4-year period, during which time this money can be brought to the UK without an additional tax charge.

Existing tax residents, who have been tax resident for fewer than 4 tax years and are eligible for the scheme, will also benefit from the relief until the end of their 4th year of tax residence.

Liability to inheritance tax (IHT) also depends on domicile status and location of assets. Under the current regime, no inheritance tax is due on non-UK assets of non-doms until they have been UK resident for 15 out of the past 20 tax years. The government will consult on the best way to move IHT to a residence-based regime. To provide certainty to affected taxpayers, the treatment of non-UK assets settled into a trust by a non-UK domiciled settlor prior to April 2025 will not change, so these will not be within the scope of the UK IHT regime. Decisions have not yet been taken on the detailed operation of the new system, and the government intends to consult on this in due course.

Furnished holiday lets (FHL)

The FHL tax regime, which relates to short-term rental properties, is to be abolished from April 2025.

Currently, if an individual lets properties that qualify as FHLs:

- The profits count as earnings for pension purposes

- They can claim Capital Gains Tax reliefs for traders (Business Asset Rollover Relief, relief for gifts of business assets and relief for loans to traders)

- They’re entitled to plant and machinery capital allowances for items such as furniture, equipment and fixtures

Raising standards in the tax advice market

A consultation has been issued to discuss the government’s intention to raise standards in the tax advice market through a strengthened regulatory framework. It sets out three possible approaches to strengthening the framework: mandatory membership of a recognised professional body, joint HM Revenue and Customs (HMRC) – industry enforcement, and regulation by a separate statutory government body. The consultation also explores approaches to strengthen the controls on access to HMRC’s services for tax practitioners.

This has relevance to anyone who may receive or provide tax advice or offers services to third parties to assist compliance

with HMRC requirements. For example, accountants, tax advisers, legal professionals, payroll professionals, bookkeepers, insolvency practitioners, financial advisers, customs intermediaries, charities and other voluntary organisations that help people with their tax affairs, software providers, employment agencies, umbrella companies and other intermediaries who arrange for the provision of workers to those who pay for their services, people who engage workers off-payroll, promoters, enablers and facilitators of tax avoidance schemes, professional and regulatory bodies, and clients, or potential clients, of all those listed above.

The consultation runs until 29 May 2024.

VAT

The VAT threshold is increasing from £85,000 to £90,000 from 1 April 2024, the first increase in seven years. See our tax tables 2024/25 for more details. See our tax tables 2024/25 for more details.

If you’d like to discuss any of the changes announced in the Budget or would simply like to explore ways that you can minimise the amount of tax you pay on your wealth, why not get in touch and speak to one of our expert team of advisers. We’re offering anyone with £100,000 in savings, investments or pensions a free financial review worth £500.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate tax advice.

Hunt’s politically charged budget

Hunt’s politically charged budget gives the voting public a second National Insurance cut in six months, but will it be enough to save the Tory party in the upcoming General Election?

Chancellor Jeremy Hunt delivered what could be his last Spring Budget (on 6 March 2024), with a further 2% National Insurance cut making the headlines, but there were other measures introduced which could have an impact on your finances. So, what was announced?

Arrange your free initial consultation

National Insurance

Following the 2% National Insurance reduction announced in the Autumn Statement last November, a further 2% National Insurance reduction was announced. This will again affect earnings between £12,570 and £50,270 p.a. and will take effect in April 2024 in the pre-election giveaway that was widely anticipated following speculation in the press. This will save workers up to a further £753 p.a., on top of the up to £753 p.a. saving as a result of the reduction announced in the Autumn Statement.

Child Benefit

It was announced that the High Income Child Benefit Charge (HICBC) will be replaced by a household income based system in April 2026 following a consultation. In the meantime, from April 2024 the threshold above which the HICBC starts to apply on a tapered basis will increase from £50,000 to £60,000 and the top of the taper will increase from £60,000 to £80,000 in a move that Mr Hunt will hope will please working families.

Savings/Investments

Following speculation prior to the Autumn Statement, a British ISA was announced. This will be a further £5,000 tax free ISA allowance for investments into British companies, which will be available in addition to the standard £20,000 ISA allowance.

A new British Savings Bond will also be made available through National Savings and Investments (NS&I), which will offer a fixed rate over three years, though the rate payable has not been announced.

Pensions

Regarding the lifetime allowance, currently 0% and due to be scrapped in April 2024, there were no further changes announced. However, Mr Hunt did not miss the opportunity to reference Labour’s plans to reintroduce the allowance, stating “Ask any Doctor what they think about Labour’s plans to bring it back, and they will say “don’t go back to square one'.”

There were also new rules announced requiring Defined Contribution and Local Government pension funds to disclose how much UK equity exposure they have relative to their international equity exposure. This could prove controversial given the funds’ mandates will be to produce the best risk adjusted return they can for investors, irrespective of their asset allocation.

Property

It was announced that higher rate Capital Gains Tax (CGT) rates on property sales will be reduced from 28% to 24% in April 2024, in a move that the government claims will be revenue generating. The Furnished Holiday Lettings (FHLs) regime will also be abolished.

‘Non-doms’

The current ‘non-dom’ rules, a tax advantageous regime for those who are non-UK domiciled (their ‘permanent home’ is outside the UK), will be replaced by a residency based system from 2025.

Inheritance Tax

After strong rumours that Inheritance Tax would be scrapped before last year’s Autumn Statement, it was not mentioned in the Chancellor’s budget statement.

Conclusion

In what was always going to be a politically charged speech given the proximity to the general election, Chancellor Jeremy Hunt will hope he has done enough to convince voters to give the Conservative Party another term in office in his Spring Budget. In what the Labour Party leader Keir Starmer described as a ‘Last Desperate Act’; the speech was filled with warnings about the potential implications of a future Labour government (the budget speech transcript on the gov.uk website has ‘political content removed’ 27 times!).

However, workers, families, those selling second homes and those already benefitting from last year’s Lifetime Allowance changes may see themselves as in a better position than they were previously, and they could see a future Labour Government as a risk to the longevity of the recently announced changes.

If this is to be the case, there could be a limited opportunity to plan over the next few months. So now is the time to seek advice, to make sure you are doing all you can to protect you and your family’s wealth. If you'd like to learn more about how you can minimise the amount of tax you pay on your wealth, why not get in touch and speak to one of our experts for a free initial consultation or please speak to your adviser if you would like to discuss any of the changes detailed above.

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The opinions shared in this article are solely those of the individual and they do not necessarily reflect those of The Private Office.

The Financial Conduct Authority (FCA) does not regulate tax advice.

Arrange your free initial consultation

Don’t let redundancy derail your future

In anticipation of the first Labour budget in 14 years and repeated warnings from the Prime Minister Sir Keir Starmer that it would be ‘painful’, many companies delayed financial decisions in an attempt to mitigate any potential fallout ahead of the day. This included hiring and investment freezes amid speculation of tax rises. These came to fruition in the form of an Employers National Insurance increase from 13.8% to 15% across the board and reducing the threshold at which companies pay it from £9,100 to £5,000 (excluding smaller companies that are eligible for the employment allowance). This was all confirmed in the 2024 Autumn Budget.

At the same time, widespread disruption from AI adoption has led to restructuring across sectors, with many firms announcing redundancies as they adapt to new technologies and changing workforce needs. The combined uncertainty of fiscal policy and technological transformation has contributed to a cautious corporate environment.

Arrange your free initial consultation

The consequences of this are yet to be fully realised. However, there were concerns raised by the British Retail Consortium, which represents the likes of Amazon and Tesco, that job losses will be ‘inevitable’, a rhetoric also echoed by many in the hospitality industry, dealing a further blow after several difficult years. This follows a string of high profile and large-scale redundancies continuing into 2025 from firms such as Ford, Dyson, and John Lewis, who collectively announced over 7,000 job cuts between January and June 2025.

These recent and ongoing events in the political and economic worlds should all serve as a reminder of the fragility of employment and the importance of having a financial plan in place, as this can provide peace of mind and some breathing room if you were to become unemployed.

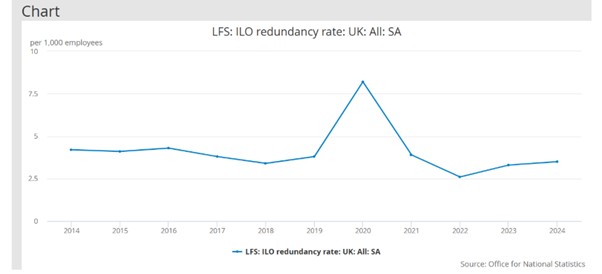

Figure 1 - UK Redundancy Rate, Source: LFS: ILO redundancy rate: UK, Q2 2025

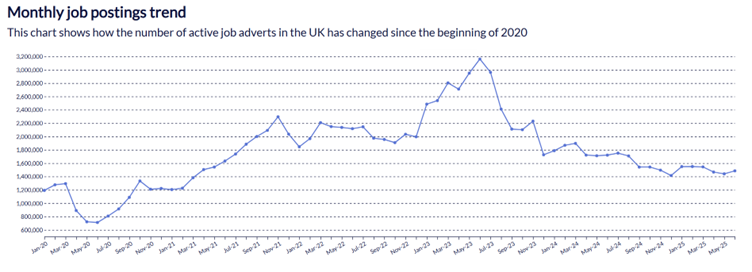

Figure 2 - Monthly job posting trends, Source: Labour Market Tracker: The REC, June 2025

How to help avoid your financial plan being derailed by redundancy

Cash emergency fund

A part of any financial plan needs to include a substantial emergency cash reserve, to ensure you are not immediately impacted by any shocks such as redundancy. As a general guide, an emergency cash fund would typically be between 3 and 12 months of income. We spend significant time with clients, using cash flow modelling, to provide answers around the size of your cash fund and how to build this buffer.

In turn using cash flow modelling and sticking to a financial plan, built with your adviser, you should have the comfort and reassurance that if a shock such as redundancy was to occur, you have built savings and investments to sustain you during such a period.

When you are made redundant

Although redundancy is a shock to your financial plans and typically seen as a negative, it can also present an opportunity for those approaching retirement.

One of the opportunities which may present itself is to make use of your redundancy payment as a contribution into your pension (up to your annual allowance or carry forward allowance). If you are close to retirement, it is an effective way of increasing the value of your pension pot with tax relief, before you potentially look to draw on it, in a tax efficient manner.

In some cases, redundancy can actually open the door to an earlier retirement than previously planned. If you have already built up a solid financial base, including pensions, ISAs, general investments, or property, a significant redundancy payout, may mean that a phased or full retirement becomes feasible. With the right planning and advice, it’s possible to assess whether your financial assets, along with your redundancy payment, could fund your lifestyle without the need to return to work.

For those who are younger when they experience redundancy, during the critical ‘accumulation’ stage of the financial plan, redundancy can point to the importance of having a financial plan and initiating these conversations with an adviser. Furthermore, typically those who are made redundant and are able to find new employment fairly quickly, there is an opportunity to implement a new refreshed financial plan to protect against any future shocks, which once again can we modelled within cash flow.

Remember, a drop or complete stop in both you and your employer’s pension contributions could seriously affect your financial plans, not least if this also includes a stop on any other benefits you may have received from your employer, such as a company car, phone or health benefits that may need to be replaced.

So, it’s really important you take the opportunity to step back and re-evaluate the financial plans you have for the future, especially if you don’t get back into employment fairly quickly.

Redundancy payment

A redundancy payment is treated as taxable income over the £30,000 tax free allowance. This payment therefore provides an amount to protect the employee from any initial cashflow problems. In terms of options for this payment there are many. As mentioned above you could contribute to your pension, which is especially tax efficient for those approaching retirement at the point of redundancy. However, there are other options as well. For instance:

- Make an overpayment/pay off a mortgage; this is a potential option to make your wider situation more secure and provide some additional comfort in a time of uncertainty.

- Hold the payment in cash accounts and draw on the money where appropriate to ensure you remain stable; this means ensuring your cash is earning the best interest is critical, particularly with top instant-access savings accounts now offering rates of up to 5% as of July 2025. Please see our , please see our Best Buy Tables

The benefit of receiving advice

Conducted by one of our experienced financial planners, cash flow modelling provides you with clarity on your current financial position and what it might mean for the future.

It simply lays out all of your income and expenditure to map out your financial future. The earlier you seek advice and begin implementing a plan the more robust your situation will be to ride out any financial shocks such as redundancy. Having a clear plan with your finances is proven to be beneficial in the long run, and with our clients at TPO we utilise cash flow modelling to give them the comfort in case of redundancy or any other similar financial shock.

If you’d like to speak to an independent financial adviser about your own personal financial plans, whether you’re concerned about redundancies or not, then why not get in touch. We can map out your financial future so you have the confidence that your wealth will last you for as long as you need it.

Arrange your free initial consultation

The financial conduct authority (FCA) does not regulate cash flow planning.

Investment returns are not guaranteed and you may get back less than you originally invested.

Past performance is not a guide to future returns.